Emergency Fund Calculator

Your Target

What Counts as an Emergency

- ✔️ Loss of income due to redundancy or illness

- ✔️ Urgent medical/dental costs not covered by NHS

- ✔️ Essential home/car repairs that prevent work

- ❌ Replacing a broken phone

- ❌ Last-minute trips or new TV purchases

*Emergency funds should never be used for non-essential expenses. This calculator assumes your essential expenses are accurately calculated.

Life doesn’t ask for permission before it throws you a curveball. A sudden job loss. An unexpected medical bill. A car breakdown that leaves you stranded. These aren’t hypotheticals-they’re realities faced by men who thought they were prepared. The difference between those who weather the storm and those who drown? An emergency fund. Not a luxury. Not a suggestion. A non-negotiable pillar of financial maturity.

What an emergency fund really is

An emergency fund isn’t a vacation stash. It’s not a side fund for that new watch or weekend getaway. It’s your financial firewall. A dedicated pool of cash, kept separate and untouched, designed to cover essential living expenses when income disappears or unforeseen costs arise. Think rent or mortgage, utilities, groceries, basic transportation-nothing more, nothing less.

It’s not about having a large balance. It’s about having enough to keep you steady while you regain control. For most men in stable employment, three to six months’ worth of core expenses is the target. If your income is irregular-freelancer, contractor, entrepreneur-aim for six to nine months. The goal isn’t wealth. It’s peace of mind.

Why men overlook it

There’s a quiet pride in self-reliance. Many of us believe we can handle anything on our own. We’ve built our careers, maintained our discipline, kept our appearance sharp. So why should we worry about money? The truth? Discipline in one area doesn’t guarantee resilience in another. Financial fragility doesn’t show up in your reflection. It shows up in your stress levels, your sleep, your relationships.

Another reason? We confuse liquidity with luxury. We see savings as something to unlock-something to spend when we’ve earned it. But an emergency fund isn’t a reward. It’s insurance. Like a good suit: you don’t wear it to impress. You wear it because you never know when you’ll need to walk into a room and command respect.

How to build one, step by step

Start small. Don’t wait until you have a windfall. Begin with what you have today.

- Calculate your essential monthly expenses. Add up rent, insurance, groceries, fuel, phone, minimum debt payments. Don’t include dining out, subscriptions, or hobbies. Be honest. If you’re unsure, look at three months of bank statements. The average UK household spends between £1,800 and £2,500 per month on essentials. Adjust for your lifestyle.

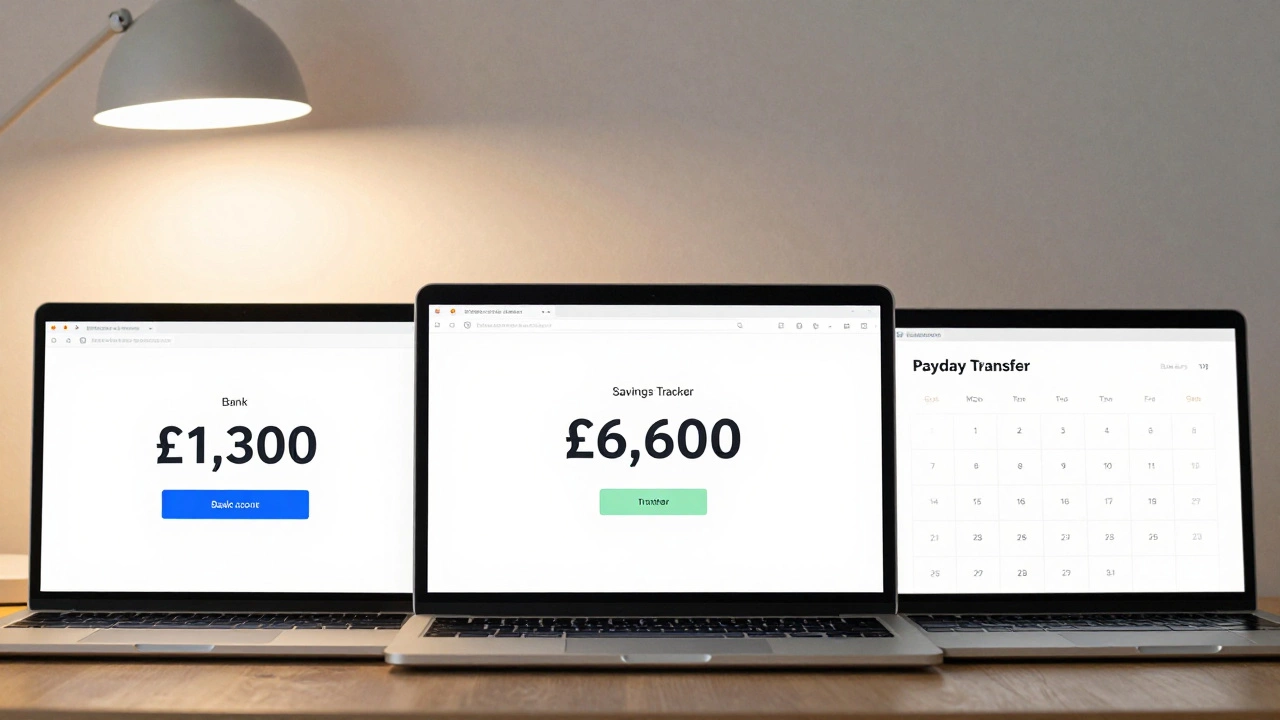

- Set a realistic target. Multiply your monthly essentials by three. That’s your minimum. Six months is your goal. If you earn £2,200/month, aim for £6,600 to £13,200.

- Open a separate savings account. Not just a different folder in your main account. A truly separate account-at a different bank if possible. This removes temptation. Name it something neutral: "Emergency Reserve" or "Stability Fund." Avoid names like "Fun Money" or "Holiday Cash."

- Automate the deposit. Set up a direct debit to transfer £50, £100, or £200 every payday. Even £25 a week adds up to £1,300 a year. Consistency beats intensity. You don’t need to save big. You need to save often.

- Use windfalls wisely. Tax refunds, bonuses, side income-don’t let them vanish into upgrades or experiences. Allocate at least half to your emergency fund. This is where discipline becomes legacy.

Where to keep it

Your emergency fund needs to be safe, accessible, and earning something. Not high-risk. Not locked away. Here’s what works:

- High-yield savings accounts. These are the gold standard. They offer better interest than standard accounts, with instant access. Look for ones with no withdrawal penalties. In the UK, providers like Nationwide, Monzo, or Starling offer competitive rates.

- ISAs with instant access. A Cash ISA gives you tax-free growth. Perfect for long-term building. You can contribute up to £20,000 annually.

- Avoid: Stocks, crypto, fixed-term bonds, or accounts with withdrawal notice periods. If you need the money in 48 hours, it shouldn’t take 14 days to access.

The key is liquidity. You’re not investing. You’re preserving.

What counts as an emergency

This is where most people go wrong. An emergency fund isn’t for:

- Replacing a broken phone

- Going on a last-minute trip

- Buying a new TV

- Missing a credit card payment

It is for:

- Loss of income due to redundancy or illness

- Urgent medical or dental costs not covered by the NHS

- Essential home or car repairs that prevent you from working

- Unexpected legal or childcare emergencies

Ask yourself: If I lost my income tomorrow, would this expense keep me from feeding my family or keeping a roof over my head? If yes, it’s an emergency. If no, it’s a choice-and choices should come from surplus, not survival.

What happens when you don’t have one

Men without emergency funds don’t just get stressed. They get trapped.

You take on high-interest debt. You raid pensions early. You borrow from friends and feel shame. You delay medical care. You lose sleep. You become reactive, not strategic. Your confidence erodes-not because you failed, but because you were unprepared.

Consider this: In 2025, the Bank of England reported that 38% of UK working men had less than £500 in accessible savings. That’s not a buffer. That’s a liability waiting to be triggered.

Building an emergency fund isn’t about being cautious. It’s about being in control. It’s about knowing that if tomorrow brings disruption, you won’t have to scramble. You’ll have a plan. And a plan, in the hands of a disciplined man, is power.

Start today

You don’t need to save £10,000 tomorrow. You just need to start. Open the account. Set the transfer. Let it grow quietly, like a well-tailored coat you keep in the closet-ready, not for show, but for when the weather turns.

Financial resilience isn’t flashy. It doesn’t make headlines. But it’s the quiet foundation beneath every great life-whether you’re leading a team, raising a family, or simply standing tall in a world that rarely pauses for anyone.